Trans Mountain, with its pipeline threatened in Jasper wildfire, has long said wildfire risk is ‘low’

Despite a wildfire risk deemed ‘low,’ the Trans Mountain pipeline ended up among ‘critical infrastructure’...

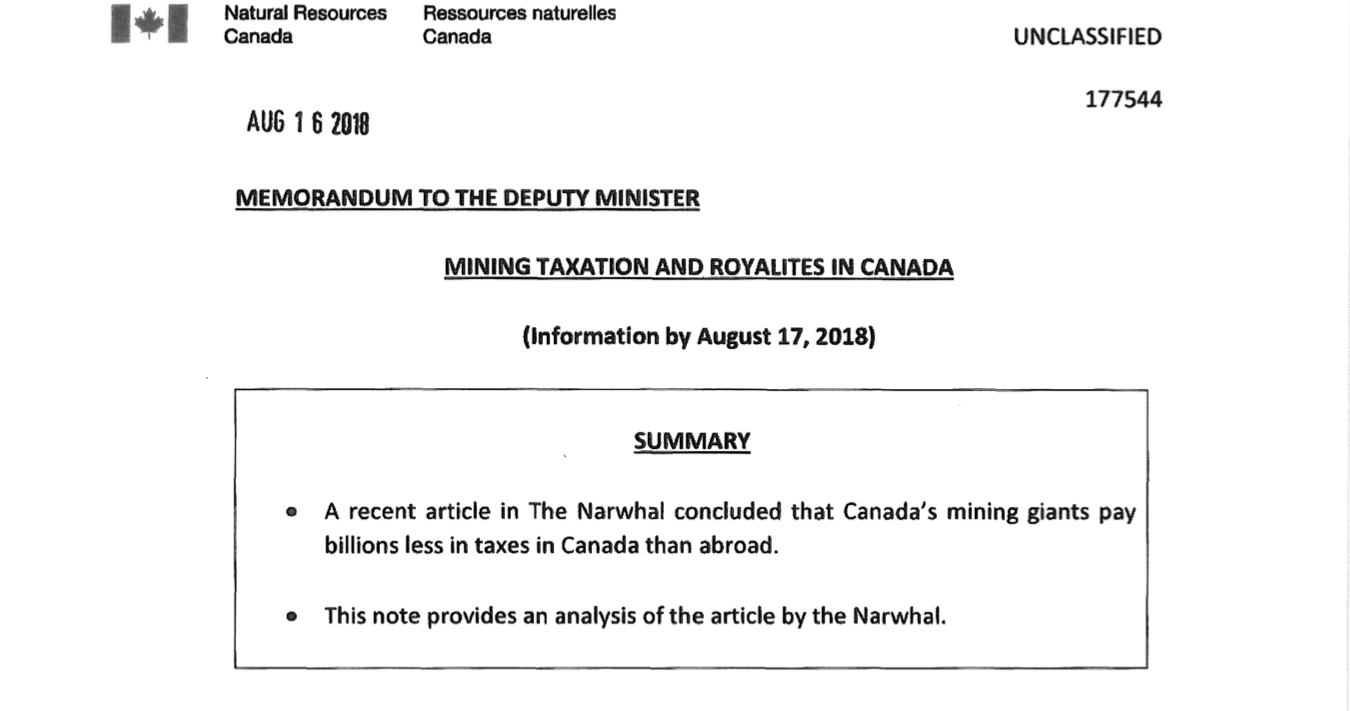

Canada’s Ministry of Natural Resources produced an internal memo in response to The Narwhal’s July 2018 investigation into gold mining taxes and royalties, a freedom of information request reveals.

The investigation, which compared mining payments in Canada to similar payments abroad, found Canadian governments were collecting far less than they could per ounce of gold extracted.

A month after the article was published, Glenn Mason, the assistant deputy minister for Natural Resources Canada’s land and minerals sector, submitted a memo to the department’s deputy minister that “provides an analysis of the article by The Narwhal.”

The memo relates details from The Narwhal’s investigation, including discrepancies between taxes and royalties paid by mining company Barrick Gold in Canada when compared to what it paid in the Dominican Republic.

In 2017, Barrick Gold extracted $250 million in gold from Ontario’s Hemlo mine while paying only $14.4 million — 5.8 per cent of the gold’s worth — in royalties and taxes. By comparison, the company extracted $817 million in gold from its Pueblo Viejo mine in the Dominican, paying $327 million — 40 per cent — of the gold’s worth — in taxes and royalties.

While much of the four-page memo was redacted, two experts asked by The Narwhal to review the document said it reveals a great deal about how government has acclimatized to low tax rates for mining.

Andrew Bauer, a natural resource governance consultant formerly with the Natural Resource Governance Institute, said the memo offers an inside view of the government’s understanding of the industry.

“With all due respect to the staff at Natural Resources Canada who drafted the letter, there is an urgent need to improve Canadian public officials’ understanding of oil, gas and mining project financing and fiscal regimes, both at the federal and provincial levels,” Bauer told The Narwhal after reviewing the memo.

Screenshot of the internal memo prepared for Natural Resources Canada’s deputy minister.

The main concern voiced in the memo was that the Extractive Sector Transparency Measures Act (ESTMA) database The Narwhal used to assess payments doesn’t include information about production costs or profitability of mines.

“The cost per ounce of gold produced can vary significantly in different mines and countries,” Mason wrote in the memo. “A higher cost means a lower profit margin and a lower ‘ability to pay.’ ”

Mining royalties in Canada are determined based on profits. That’s different from many other countries, which apply them based on production.

Canada uses profits to assess royalty schemes, but does not require companies to disclose numbers on profitability in the ESTMA disclosure database, which was launched in 2015. The database, Canada’s primary transparency mechanism for extractive companies, is still in its infancy and does not require companies to report information in a consistent manner.

In order to report on mining tax and royalty regimes and compare them to other jurisdictions, The Narwhal scoured annual reports of gold mining companies to provide a detailed breakdown of a mine’s “all-in sustaining cost” — an industry metric used to report production costs on a per-ounce basis.

The memo overlooked this original information gathering, which adds contextual analysis to the ESTMA data.

Pointing to Canada’s production costs isn’t a justification for low tax and royalty rates, according to Bauer, who suggested the argument about differing production costs is a distraction from the fundamental problem with Canadian tax and royalty frameworks.

Mine profitability around the world is dependent on many factors, Bauer said, not just the cost of production. Those factors include things like quality of the deposit, price of the commodity and financing costs.

Ugo Lapointe, long-time mining watchdog and coordinator for MiningWatch Canada, said companies that invest in Canada are well aware of high operational and labour costs — but are undeterred because of that high profit potential.

What’s most relevant, Lapointe said, is how little the Canadian public knows about mining costs and payments, in general.

“There is no transparency on this in Canada.”

The ESTMA database has only released piecemeal data self-reported by companies for 2016 and 2017.

“Arguments that higher operational and labour costs cut into profits for Canadian mines versus international mines remain to be proven with facts and figures,” Lapointe added.

An inequity may be baked into the very way we do mining in Canada, according to Bauer.

Private mining companies are designed to extract and sell as much mineral, say gold, as possible in a given year, even if overproduction means they aren’t fetching the best prices, Bauer added.

That means these minerals — non-renewable assets — are being sold off for much cheaper than if production was restricted until prices were higher and could guarantee better returns for the owners of the resource: Canadians.

Bauer also noted that mining is location-specific, which should allow governments to collect far more in revenue when compared to more mobile sectors like tech.

Percentage of fees paid per ounce of gold extracted at projects owned by three companies that operate in Canada and abroad. Source: Extractive Sector Transparency Measures Act. Graphic: The Narwhal

A gold deposit, unlike a factory, can’t move to a neighbouring jurisdiction where taxes and royalties are more favourable. High-quality deposits are relatively rare, meaning governments can ensure that the owners, its citizens, are getting full value.

“Would you sell your house cheaply and declare success?” Bauer asked.

“This approach is especially problematic since these resources are non-renewable, so if the asset is sold cheaply today, the lost revenue can never be recovered.”

A 2011 information bulletin from Natural Resources Canada reported that Canada collects considerably less in taxes and royalties than Australia, Indonesia, Peru, Tanzania or South Africa.

According to the bulletin, at a 15 per cent internal rate of return, a mining project in Canada pays an average effective tax rate of 22.5 per cent. That’s compared to 60.9 per cent in Peru, 74 per cent in Indonesia or 79.8 per cent in Western Australia.

In the memo, Mason notes this is in part because, “as an advanced economy, Canada receives more personal income tax revenue than corporate income tax revenue.” (Mason also notes that the “ESTMA database does not include source deductions paid by workers at a mine” so “the payment information is incomplete.”)

But Bauer said this comparison of personal versus corporate income tax is a “false dichotomy.” There’s no required trade-off between income tax from workers and that from companies. Both can happen.

Lapointe added that those figures don’t include a number of factors that further reduce the Canadian government’s take, including what Lapointe describes as “very generous direct and indirect subsidies.”

All tax breaks, flow-through shares, infrastructure spending and low securities for clean-up are instances where governments are effectively boosting the profitability of mines by requiring companies to pay less. Other such generous provisions include tax-deductible royalty payments, accelerated depreciation of capital assets and the carrying forward of tax credits and operating losses for up to 20 years.

Bauer said there may be a case for gifting such incentives to small exploration companies but “they make absolutely no sense” for large transnational mining companies.

Bauer notes that Canada’s mining sector comes with a series of key advantages to companies: a skilled workforce, established transportation networks, political stability and low electricity and water costs. As a result, he suggested that fiscal incentives like lower taxes and royalties aren’t necessary to entice investment.

Lapointe said the memo, presented to the deputy minister to add context to The Narwhal’s reporting, doesn’t touch on the way Canada works to attract investment from the mining industry.

“The memo makes no allusion to these direct and indirect subsidies,” he said.

The memo also didn’t address the practice of “base erosion and profit shifting,” which The Narwhal’s original article referenced.

The OECD defines this as “tax avoidance strategies that exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax locations.”

Lapointe says this practice is arguably “the biggest fiscal issue around mining in Canada.”

Due to a lack of government data it isn’t possible to say how prevalent the practice is, although there is evidence of it occurring in several instances.

The Canada Revenue Agency (CRA) attempted to bring charges against Saskatchewan-based uranium behemoth Cameco for shifting profits to a European subsidiary. A CRA audit found profit transfers during 2003, 2005 and 2006 would have added an additional $484.4 million to Cameco’s income.

According to accounting firm Grant Thornton, the Tax Court of Canada’s decision on the Cameco case “dealt a serious blow” to the CRA’s attempts to curb the practice.

Other mining companies that have been hit with accusations of tax avoidance include Silver Wheaton and Turquoise Hill Resources.

Despite all this, the memo assured the deputy minister of Natural Resources Canada that the country “has been recognized on an international basis as sound and efficient.”

Bauer said that position is supported by industry lobby groups, such as the Mining Association of Canada, but is not based on independent assessments.

“The statement from Natural Resources Canada demonstrates a failure to carry out independent analyses,” he told The Narwhal.

As an example, Bauer pointed to a 2013 report from the University of Calgary’s School of Public Policy, which recommended that provinces “start eliminating preferential and wasteful tax breaks for miners,” as “provincial treasuries certainly cannot afford these breaks, and neither can the Canadian economy as a whole.”

Mining also creates a notoriously low number of jobs per dollar invested — similar to oil and gas extraction — and automated trucking may further reduce employment opportunities.

There are 255 mines in Canada that a recent report by the Office of the Auditor General found are not adequately regulated.

Mines can also cause long-term impacts on the environment, as seen with the Mount Polley tailings disaster or Elk Valley mines in B.C. Mines can represent costly long-term liabilities that are often left to taxpayers, as with the Tulsequah Chief mine in B.C. or the Giant mine in the Northwest Territories.

NRCan Memo on Mining Taxation Royalties Canada by The Narwhal on Scribd

For months on end, buses and SkyTrain cars all over Metro Vancouver were wrapped in ads declaring “B.C. LNG will reduce global emissions.” Memo to...

Continue reading

Despite a wildfire risk deemed ‘low,’ the Trans Mountain pipeline ended up among ‘critical infrastructure’...

As Jasper wildfires make international headlines, our awe for the storied place transcends political parties,...

A provincial spill report details a list of issues that arose as crews responded to...